Can I pass down my Limited Liability Partnership (LLP)?

The information in this article applies specifically to limited liability partnerships.

For details on sole proprietorships, please refer to our article on sole proprietorships.

For details on private companies, please refer to our article on private companies.

TLDR version: This would largely depend on the partnership agreement. Assuming there are no specific arrangements, you can only pass down your interest in the LLP up to the point of your demise.

What is an LLP?

A Limited Liability Partnership (LLP) is a vehicle for doing business in Singapore. An LLP gives owners the flexibility of operating as a partnership while having a separate legal identity like a private limited company. An LLP is capable of, amongst other things, acquiring and holding property in its name.

Can I pass down the assets belonging to the LLP?

Assets belonging to the LLP do not form part of the deceased’s estate and therefore cannot be distributed directly via the Will. The assets will continue to belong to the LLP.

Can I then “pass down” my “partnership”?

In private companies, you own shares in the company, whereas in a sole proprietorship you own all the assets of the business. However, in an LLP setting, when a partner dies, they cease to be a partner. You cannot give away your LLP interest in the same way as you can with shares in a company or the assets of a sole proprietorship.

Barring any separate partnership agreements, by default you may only pass on your interest in the LLP (capital, profits, rights to accounts) to your beneficiaries.

What do you mean my interest in the LLP?

Limited Liability Partnerships (LLPs) are subject to partnership agreements that govern the rights and duties of partners. In the absence of such an agreement, the First Schedule of the Limited Liability Partnerships Act applies, under which all partners are entitled to share equally in the capital and profits of the LLP.

Similarly, the LLP Act also determines what happens in various matters unless an agreement between the partners states otherwise. For example, according to section 15 of the LLP Act, a partner ceases to be a partner upon death, and his estate is entitled to receive from the LLP an amount —

(a) equal to the former partner’s capital contribution to the LLP and the former partner’s right to share in the accumulated profits of the LLP after deduction of losses; and

(b) determined as at the date the former partner ceased to be a partner.

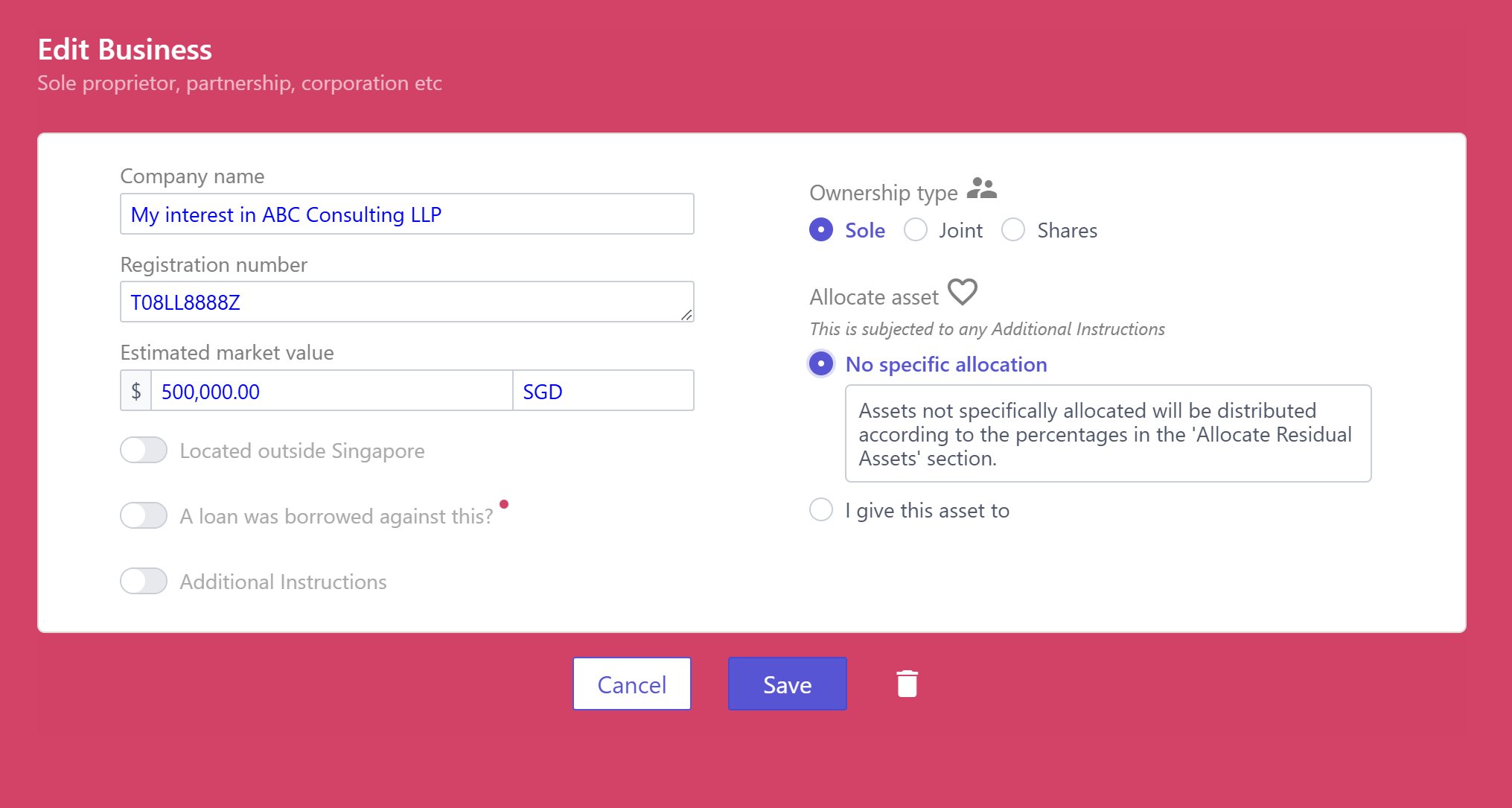

How do I list my interest in the LLP?

Within the platform, under “Allocate Assets”, you can list it in the “Business” category as “My interest in {Name of LLP}”. Under "Ownership type", select "Sole" as you are referring only to your interest in the LLP.

Can I dictate who will replace me as a partner upon my demise?

The admission of a new partner requires the agreement of the remaining partners and compliance with the LLP agreement. You also cannot directly appoint your successor partner through your Will. If you want a specific person (e.g. a child or spouse) to step in as a new partner, your surviving partners must agree — either through the partnership agreement drafted beforehand or by mutual agreement of the remaining partners in the absence of one.

Every limited liability partnership must have at least 2 partners. If there are fewer than two partners left for a period of more than two years, then the remaining partner carrying on the LLP is personally liable, jointly and severally with the LLP, during the period after those two years (section 28 of the LLP Act).

What about business succession planning with a LLP?

Given the complexities, if succession beyond the current partners in the LLP is something you want, you should consider converting the LLP to a private company (limited by shares), where (again barring any other agreements) you will be able to transfer your shares, making the beneficiary a shareholder of the company.

Alternatively, you can amend the LLP Agreement itself to state what happens on the death of a partner, e.g. granting the deceased partner’s nominee a right to be admitted.